COVID cancellations: is your trip covered?

*Advertisement feature*

Like many things, travel in the post-COVID ‘new normal’ is going to be slightly different to what we were used to before, for a while at least.

Staycations are the hot new trend, masks are required on planes and trains, and if you do decide to brave a trip abroad, it’s all about watching out for air bridges and hoping you don’t need to quarantine on arrival back home.

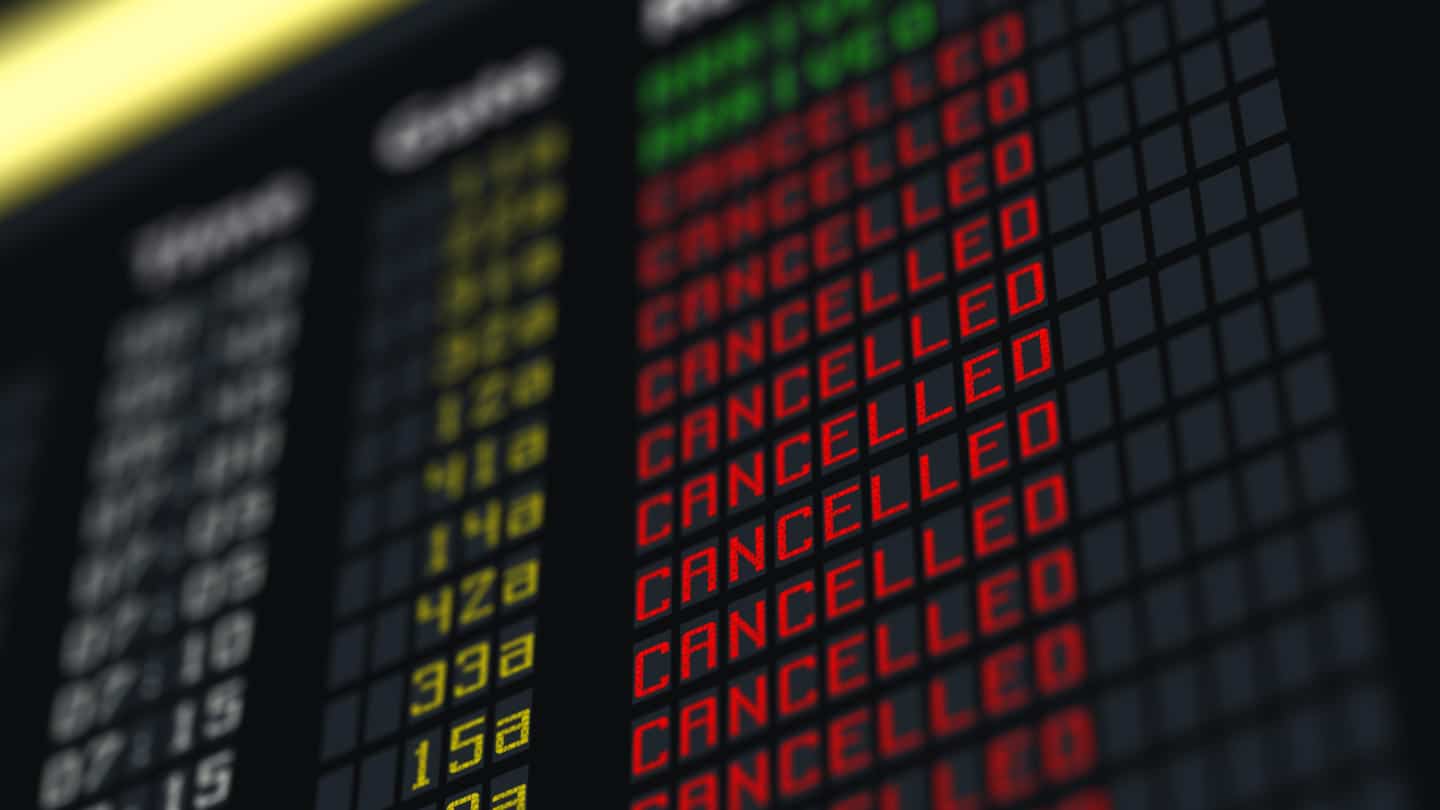

Another reality we have to learn to live with is that our best-laid plans may end up being cancelled, perhaps with very little warning. No one can predict with any certainty exactly when local spikes are going to lead to sudden lockdowns, or how arrangements between countries are going to shift.

Here’s what travel experts are saying about booking holidays now.

If you have flights and accommodation booked in a certain destination and it imposes lockdown measures before you arrive, there is very little you can do. The big question many travellers are facing in situations like this is – what do you do about getting your money back?

COVID-19 travel cancellations have exposed what is a real grey area in consumer rights regulations. If you want to read up on your chances of getting your money back, let us save you some time – the conclusion you will reach is that you might be able to claim some of your money back, but then again you might not.

Your best chances are if you had booked a package holiday, or if you had booked a flight with an airline from an EU member state (the EU has very generous consumer protection laws). But even then, you may be offered rescheduled flights or vouchers rather than a monetary refund, which might not be convenient.

Insurance gives you certainty

The only way to be certain of getting your money back for a COVID-related cancellation is to have travel insurance. Not only will a good policy cover your losses should your airline or accommodation provider have to cancel, it also protects you if you decide the risk of going is too high and change your mind.

In the past, travel insurance has been treated like an optional extra by too many people heading abroad. But even with staycations, the risk of cancellations means everyone really should be treating it as an essential item on their planning list.

With potential cancellations in mind, it is important to make sure you get the right level of cover with your travel insurance. Basic policies might look attractive because they are cheap, but you should check the small print to find out exactly what level of cover you get for cancellations, and to what value.

Bear in mind that cheaper policies will often have an excess to pay on a claim, so you will end up losing money should your trip not go ahead either way. The safest bet is to take out comprehensive cover, which should protect you against cancellations no matter the circumstances.

Finally, COVID has increased the risks for insurance companies too, and you may find this results in your insurer putting up prices or withdrawing certain products. We’ve also seen a spate of non-insurance specialists, such as large retailers and banks, decide to pull out of the travel insurance market. If you were a John Lewis Travel Insurance customer, for example, you will need to look for a new provider. In the current circumstances, you would be best advised going for a specialist travel insurance provider.

Disclosure: this is a guest post is advertorial content.